For any economy to prosper there is a mixture of optimally used ingredients which drives its growth rate. A million dollar question which lies in the path of every economist in a country is how to maintain an optimal balance between growth (i.e. rise in GDP) & welfare. One factor which is common to both of them is `RATE OF SAVINGS`. If we look at the past trends of the Indian economy one of the major factor that was responsible for increased economic growth was sustained increase in household savings & investments. Similarly from welfare point of view high household savings lead to better or improved standards of living as they cushion the individuals from unforeseen detrimental consequences.

For any economy to prosper there is a mixture of optimally used ingredients which drives its growth rate. A million dollar question which lies in the path of every economist in a country is how to maintain an optimal balance between growth (i.e. rise in GDP) & welfare. One factor which is common to both of them is `RATE OF SAVINGS`. If we look at the past trends of the Indian economy one of the major factor that was responsible for increased economic growth was sustained increase in household savings & investments. Similarly from welfare point of view high household savings lead to better or improved standards of living as they cushion the individuals from unforeseen detrimental consequences.

These past trends gives us a clear understanding of the key that can lead to growth as well as welfare taking place simultaneously in the economy and that is to set policies which can increase the savings rate of the country. We all will be shocked by the fact that only a little more than 50% of Indian own a savings bank A/C. The reasons are very obvious and simple. There are simply 27 public banks and 22 private banks. The new CRISIL Inclusix index on financial inclusion says that the bottom 50 districts have just three banks per 100,000 of population which is very less. Moreover most of the banks require high initial sum of money to open a savings A/C and the minimum amount which should always be there in the A/C is also quite high as the population of our country below poverty line is quite high i.e 27cr.

Few firms who realized that there was a gap in government policy took an initiative to fill up this gap. In broad terms these firms are known as the `MICROFINACE` Company`s. Microfinance is a source of financial services for entrepreneurs and small businesses lacking access to banking and related services. The two main mechanisms for the delivery of financial services to such clients are: (1) relationship-based banking for individual entrepreneurs and small businesses; and (2) group-based models, where several entrepreneurs come together to apply for loans and other services as a group.

Few firms who realized that there was a gap in government policy took an initiative to fill up this gap. In broad terms these firms are known as the `MICROFINACE` Company`s. Microfinance is a source of financial services for entrepreneurs and small businesses lacking access to banking and related services. The two main mechanisms for the delivery of financial services to such clients are: (1) relationship-based banking for individual entrepreneurs and small businesses; and (2) group-based models, where several entrepreneurs come together to apply for loans and other services as a group.

BANDHAN is one such company that tries to bridge this gap. The Kolkata-based microfinance company with 45 branches and a customer base of 2.6 million in unbanked rural areas has roped in consulting firm Deloitte to help with the application. It was set up to address the dual objective of women empowerment & poverty alleviation. Their mission is very clear to them and that is to reduce socio -economic poverty substantially and create employment by targeting low income households across the country through providing cost effective sustainable financial & non- financial services focusing on social securities.

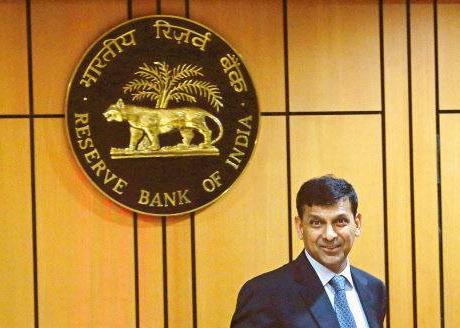

You must be wondering how such a small microfinance company at micro level can help the aggregate savings rate of the country to be enhanced at the macro level. This gap has been filled efficiently by the Governor of RBI Mr. `Raghuram Rajan` and the committee headed by former governor Bimal Jalan C.B. Bhave, former chairman of Securities and Exchange Board of India (Sebi); Nachiket Mor, RBI’s central board member; and Usha Thorat who is former RBI deputy governor, met in New Delhi to finalize the list.Out of 25 giant corporations who had applied for this new banking license IDFC, an infrastructure finance firm and Bandhan Financial Services, a micro-lender to the poor were selected. This new strategy adopted by the governor of rejecting other various billionaire companies who were also competing for this new license can be a step forward to enhance the living conditions and income of the rural population of our country. The already established banks have no experience in dealing with rural and semi – rural customers as the financial requirements of these people are very small and limited. Moreover their knowledge about finance and loan is very limited hence their needs and requirements cannot be catered by these big corporate banking companies. For example if a farmer needs loan to get his house repaired HDFC bank or HSBC cannot help that poor guy because his requirement of loan does not match their minimal loan standards. In order to make these financial facilities penetrate the rural masses it was essential to bring a microfinance company as `BANDHAN` on its front foot as this company already has experience to fulfill the needs of the target audience in East India region hence recognizing them on national front will help in stretching their means all throughout the country.

You must be wondering how such a small microfinance company at micro level can help the aggregate savings rate of the country to be enhanced at the macro level. This gap has been filled efficiently by the Governor of RBI Mr. `Raghuram Rajan` and the committee headed by former governor Bimal Jalan C.B. Bhave, former chairman of Securities and Exchange Board of India (Sebi); Nachiket Mor, RBI’s central board member; and Usha Thorat who is former RBI deputy governor, met in New Delhi to finalize the list.Out of 25 giant corporations who had applied for this new banking license IDFC, an infrastructure finance firm and Bandhan Financial Services, a micro-lender to the poor were selected. This new strategy adopted by the governor of rejecting other various billionaire companies who were also competing for this new license can be a step forward to enhance the living conditions and income of the rural population of our country. The already established banks have no experience in dealing with rural and semi – rural customers as the financial requirements of these people are very small and limited. Moreover their knowledge about finance and loan is very limited hence their needs and requirements cannot be catered by these big corporate banking companies. For example if a farmer needs loan to get his house repaired HDFC bank or HSBC cannot help that poor guy because his requirement of loan does not match their minimal loan standards. In order to make these financial facilities penetrate the rural masses it was essential to bring a microfinance company as `BANDHAN` on its front foot as this company already has experience to fulfill the needs of the target audience in East India region hence recognizing them on national front will help in stretching their means all throughout the country.

This differential banking system can prove to be a success only if these companies stick to their goals and missions of eradicating poverty. Recognizing them as `Nationalized Bank` is a great opportunity for a microfinance company as now they are in a position to offer full-fledged bank services to the poor. Now it`s in their hands whether they take full advantage of this situation or just prove to be old wines in new bottles.

This differential banking system can prove to be a success only if these companies stick to their goals and missions of eradicating poverty. Recognizing them as `Nationalized Bank` is a great opportunity for a microfinance company as now they are in a position to offer full-fledged bank services to the poor. Now it`s in their hands whether they take full advantage of this situation or just prove to be old wines in new bottles.

{kind=link}