Throughout our lives, we have been hounded by the dire need for money that runs our world’s entire clockwork and it is only fair for the youth to cry out for ways to earn it. Often we see many countries being metaphorically crushed to the ground due to enormous debts.

Greece has been a world-renowned culprit of suffering due to extremely bad debts, or it may just be a PR stunt where tourists were enticed into visiting the place out of sheer pity.

These debts mostly racked up owing to them being indebted to a flurry of countries and the juggernaut, World Bank.

Thus, as you are introduced to the enormous scale to which bad debts can affect an entire nation, let alone an individual, it must be ensured that we do not bite more than we can chew. That is where our schools fail us.

We fail to entirely understand the process of loaning and uncapped loaning. But, fear not, for here we bring to you a step-by-step breakdown of how to file for a loan and make it one that does not end up with you conceding a bad debt.

Zero In On The Amount Of Money You Actually Need

You need a loan for your education but you think that you may require a little extra as well, so you think of adding another twenty grand as your final loan amount and you jot it down.

However, during this entire course of brainstorming, you never accounted for the amount you could keep as collateral or the possibility of you being able to pay the amount back when you start earning.

This scenario presents us with a strange dilemma, especially when we are trying to get into a college for which we may not want to dip our hands in our parents’ wallets. The first step to growing up is to realize the capability of our target degree in securing a well-paying fresher job.

The value of our collateral comes into play as well but not until later. Thus, it always pays to go for a loan that you can pay off with relative ease.

List Down Banks Alongside The Interest Rates

It obviously goes without saying that we need to choose banks as per the interest rates and the moratorium period, or the period during which we are absolved of paying any form of money to the bank. Yet, most of us fail to understand the need to optimally decide upon a bank for our own safety net to fall back upon.

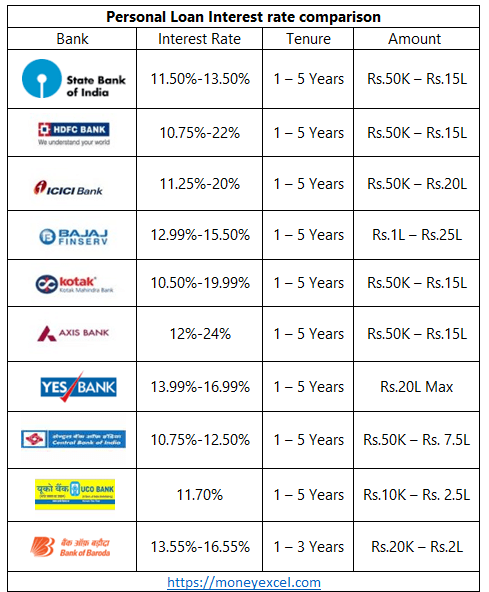

Most banks in the public sector charge an interest rate of 7.6% for an Education Loan which may rise up to 10.6% while private sectors may charge a rate of 10% which may rise up to 16%.

The interest rates at private banks vary with each bank hence, it’s always difficult to zero in on one. For personal loans, on the other hand, the rate of interest is comparatively higher than education loans as it usually starts from 10% rising to about 16% in the public sector.

Thus, it is always important to zero in on where you will get your loan from, and also, this is where your target loan amount comes into play.

It must be stated, without any bias, that private banks are much more accountable especially in this day and age where public banks are being merged or being dissolved.

Also Read: Life Skills They Don’t Teach In School: How To Pay Utility, Credit Card Bills

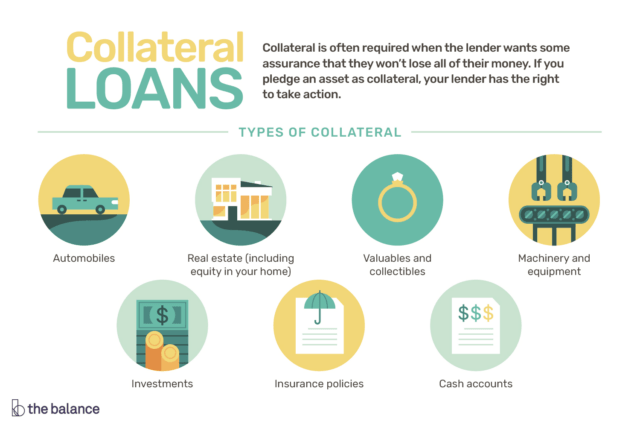

Decide Upon Your Collateral

Most banks ask for collateral to be kept as security with the bank to equal the amount of the loan taken. Some banks, especially for student loans or education loans, choose to not keep a clause for collateral; however, for ones that do, this step is for them.

Your loan may be of five lacs and thus, to equal that loan amount the bank will ask for a property to be kept as security.

A collateral can be anything, starting from your life insurance papers to an immovable property like an apartment, house, or land. This will have to be decided upon with the utmost consideration as it also makes or breaks your loan agreement.

Notice The Amount Of Time You Will Get To Pay The Amount Back

This is the last step that one needs to take care of as mostly all banks follow the same time period allotted for repayment. For student loans, the standard time allotted for repayment is 10 years after the moratorium period.

However, for standard loans, the entire game plan takes a different route as it depends on the plan chosen, as the repayment period may start from 10 years and end at 25. A standard or personal loan, in essence, has no cap if one has the necessary collateral. Thus, a longer period may be provided to the loanee.

Have Your Identification Papers Ready

Technically this is the last step but it’s fairly simple and something you would already know. But it is super important. Always have your identification papers and all other necessary documents at the ready. Even your guarantor’s documents will be extremely important.

This article has been written to help you ensure that you decide upon the best loan plan that suits your needs.

This is especially close to me, owing to the fact that I am a student who has taken out a student loan and trust me, I was hounded by the entire process myself. My mother helped me with it but she was new to the entire process as well.

Thus, these steps only exist to help you and another mother like mine to make the road beyond just a bit smoother while getting you to file for a loan.

Image Sources: Google Images

Sources: Bank Rate, Fullerton India, Bank Bazaar

Connect with the blogger: @kushan257

This post is tagged under: life skills, school, education, life skills our school did not teach us, life skills, skills, life, bank of india, axis bank file for a loan, icici bank, hdfc bank, ifsc code, yes bank, sbi bank, indian bank, bank of baroda, baroda bank, canara bank, union bank, yes bank share price, kotak, kotak bank, state bank, indusind bank, central bank, loan, home loan, education loan, personal loan, education loan interest, sbi education loan, education loan interest rate, education loan in india, student loan, student loan in india, sbi student loan, personal loan interest, personal loan hdfc, personal loan calculator, hdfc loan, loan calculator, hdfc, sbi loan, personal loan sbi, personal loan interest rate, loan calculator, home loan calculator, home loan hdfc, home loan interest, how to file for a loan, file for a loan

Other Recommendations:

What Did Sucheta Dalal’s Tweet Expose This Time That It Impacted Adani Companies?

{kind=link}